Scandals and rising default rates have prompted some private credit investors to withdraw their funds, forcing asset managers to limit redemptions. Does this trend pose a threat to distribution of trade and working capital assets, or is it an opportunity to refresh the sector’s approach to liquidity?

The private credit market has undergone a transformation over the last decade.

Though there is no universally accepted definition of private credit, it has traditionally been understood as non-bank lending, typically targeted at mid-market or lower-quality companies, with terms negotiated bilaterally.

These kinds of facilities took on greater significance in the wake of the 2008 financial crisis, when regulatory reforms placed far tougher restrictions on banks’ use of capital. At the same time, a long period of low interest rates left investors seeking more attractive returns. The seeds were sown for rapid growth: private credit assets under management grew tenfold over the following decade.

Since then, increased market volatility has only helped drive further expansion. Sizing the market accurately is a challenge, and estimates vary, but Morgan Stanley says in an October 2025 report that the private credit market had grown from US$2tn to US$3tn since 2020 – and would reach US$5tn by 2029.

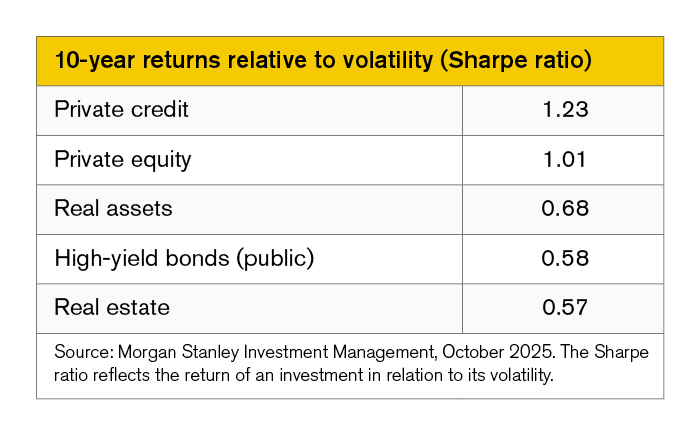

For investors, private credit has consistently offered “compelling” returns compared to traditional fixed-income investments, including high-yield bonds, private equity and real estate, Morgan Stanley says. Historical loss rates have been low, exposure to public markets is more limited than for equities and bonds, and investors often benefit from an illiquidity premium.

And though previously the realm of institutional investors, the sector’s strong performance has prompted an influx of retail investors to private credit over the last five years.

Borrowers, meanwhile, benefit from wider access to financial products and services. The Financial Stability Board (FSB) says in a May 2026 report that private credit “is essential for supporting real economic activity, particularly in underserved sectors, helping to bridge the financing gap that can exist when banks are unable or unwilling to lend”.

As a result, risk is potentially less concentrated within the banking sector, and the wider financial system can benefit from “healthy competition”, leading to better pricing and more innovation, the FSB adds.

Private credit’s expansion has also seen a wider range of underlying assets brought under its umbrella, including in trade and working capital finance. Though yields are typically lower than for term loans, which represent the lion’s share of the market, these assets boast low default rates and have grown in popularity as a source of financing – both as an alternative to bank facilities and as a supplementary line of credit.

But by late 2025, cracks in the private credit market were starting to appear.

Private credit under stress

One issue facing the private credit market is rising default rates.

Fitch Ratings said in March that its Privately Monitored Rating, which tracks defaults among US-based companies that hold private credit debt, rose to 10% in the first quarter of this year, up from around 9.2% the previous year and 8% in 2024. Of the 302 largely mid-market companies monitored by Fitch, 28 borrowers had at least one default event. The total number of defaults was 38, spread across several sectors, it said.

Another is investor concern over potential overexposure to software businesses. An April article by JP Morgan Asset Management estimates that private credit’s exposure to the software sector is around 21%, and higher if wider technology and business services sectors are included.

These assets are now seen as riskier due to the disruptive force of artificial intelligence, and though unlikely to result in “an imminent, broad-based credit default cycle”, the trend still “deserves careful monitoring”, JP Morgan says. A previous article by the bank highlighted an “abrupt and indiscriminate sell-off” of software stocks in February this year.

“Trade finance managers may not be seeing redemption pressure directly, but we can still become collateral damage.”

Bos Smith, BroadRiver Asset Management

The sector has also drawn closer attention from industry watchdogs. Though the May FSB report sets out the potential benefits of private credit, its primary focus is on potential vulnerabilities.

On the face of it, banks’ exposure to private credit funds – largely in the form of credit lines – is “relatively small”, the FSB says. However, the opaque and interlinked nature of the market means actual exposure could be higher.

There are “transparency challenges for broader monitoring of private markets”, the FSB says, because borrowers are generally not publicly rated companies and their true leverage may be obscured.

At the same time, institutions may be exposed to different parts of the private credit market. Banks may be providing revolving credit facilities to companies also borrowing from private credit funds, or insurers could be investing in funds while also providing funded reinsurance arrangements, the report says.

“This can potentially lead to difficult-to-detect pockets of risks,” the FSB says. “This layering effect may amplify losses during market stress.”

Perhaps most significantly, private credit has attracted unwanted attention following a string of high-profile scandals, including the September 2025 collapses of US sub-prime auto lender Tricolor and auto parts supplier First Brands, and more recently, the failure of UK-based mortgage lender Market Financial Solutions.

In October last year, shortly after Tricolor and First Brands had each filed for bankruptcy, JP Morgan chief executive Jamie Dimon said the sector “should be forewarned” about weak links in the private credit sector.

“When you see one cockroach, there’s probably more,” he said.

Of those three incidents, the First Brands scandal is most closely tied to trade and working capital finance. Investigators have accused the company of forging invoices and documents to obtain payables, receivables and inventory finance facilities from a host of asset management companies, with potential losses running into the billions of dollars.

Nervous investors

By early 2026, a sense of nervousness around private credit had spread to investors. Numerous funds were facing a wave of redemption requests and moved to limit withdrawals.

The Financial Times reported in April that private credit investors sought to redeem more than US$20bn in the first quarter of this year, with notable increases in requests at funds including Apollo, Ares, Barings, Blackstone, Blue Owl, Cliffwater and Morgan Stanley, among others.

Several funds responded by setting limits on withdrawals, known as gates, in part to avoid a fire sale of the underlying assets.

For funds focused on trade and working capital finance, concern seems to be coming from investors that may not be particularly familiar with the nature of the assets themselves, but who have been spooked by the negativity around the sector – particularly in relation to First Brands.

Dominic Capolongo, chief revenue officer at trade finance technology firm LiquidX, says asset managers are having to face questions from wary investors “who are lumping working capital and private credit together”.

“That’s obviously not ideal if they want immediate liquidity, but I don’t believe there is widespread panic. It’s more a function of the normal ebb and flow of that type of capital.”

René Canezin, Evolution Credit Partners

As a result, managers “are having to slow down origination of working capital, and are trying to educate investors on why it has a totally different risk profile”, he says.

Capolongo adds that there has been blowback on the corporate side too.

“We’ve heard that some corporates are looking to do more traditional financing, like a collateralised revolver with a bank, rather than a working capital facility with an asset manager – just because they’re fearful that stakeholders might be a little jumpy with all the noise around private credit,” he says. “The number of opportunities is not as abundant as it was.”

At the same time, for asset management companies under pressure to return funds quickly to investors, trade finance assets could be seen as an easier option. Working capital programmes tend to be short-term and self-liquidating, at which point capital can be redeployed or returned.

In effect, this makes them a more liquid asset compared to portfolios based around direct lending – which could have appeal in a high-redemption environment.

“We are not worried about asset impairment,” says Bos Smith, portfolio manager for US fund BroadRiver Asset Management’s trade finance strategy.

“We are worried because liquidity needs elsewhere in the private credit ecosystem can force investors to redeem from sound, performing, short-duration strategies. Trade finance managers may not be seeing redemption pressure directly, but we can still become collateral damage.”

In the scenario where funds do decide to pull capital from trade finance assets, it is “not always easier to re-enter” once investment is flowing again, BroadRiver’s Smith says.

“If you interrupt funding to a supplier, especially where the programme is part of its working capital infrastructure, you may lose the relationship,” he says.

“Investors sometimes assume trade finance can be switched off and switched back on without consequence. In reality, the programmes are relationship driven. Suppliers value reliability and availability, not just price.”

No reason to panic

But are the wobbles in the private credit market likely to have a major negative impact on investment in trade finance assets?

René Canezin, managing partner and founding partner at Evolution Credit Partners, suggests the redemption issue is “not as dramatic as it may sound”.

“The redemptions taking place appear largely related to a specific investor base, not the institutional investor base, but smaller investors such as retail, high net worth, and outsourced family office investors,” he says.

“That segment values liquidity, and private credit created products offering a degree of liquidity that attracted significant inflows. Now the market has shifted and some investors want their money back. In certain cases, they are finding that liquidity is more limited than expected.”

However, a fund that caps withdrawals does so only for the immediate period. Investors may receive only a portion of their capital back right away, but “simply need to wait longer” to redeem the rest.

“That’s obviously not ideal if they want immediate liquidity, but I don’t believe there is widespread panic,” he says. “It’s more a function of the normal ebb and flow of that type of capital.”

“We’re seeing a lot of asset managers realising that if they had a more diversified approach and more short-term working capital, they would be in better shape and wouldn’t have to slam down the gates.”

Dominic Capolongo, LiquidX

Canezin adds that while it is possible investors choose to redeem trade finance investments because they are inherently more liquid, he has “not seen evidence of that happening in a meaningful way, nor have I seen signs of widespread forced sales of underlying assets”.

Those sentiments are echoed by Nathan Feather, chief financial officer of supply chain finance platform PrimeRevenue.

“We have not seen any material changes in private credit appetite for working capital finance assets,” he says. “While there may be a bit more due diligence in the current environment, we are observing that private credit continues to be a growing source for companies to inject accretive liquidity into the working capital and trade finance markets.”

What’s next for private credit and trade finance?

A prolonged period of private credit stress and significant redemption requests over a longer period could present a challenge.

In that scenario, Canezin says, some fund managers “might need to tell clients to seek alternative financing sources”.

“But I would view that as relatively uncommon, particularly given that many asset managers operate multiple funds and have sufficient capital flexibility,” he says.

In practice, industry participants expect the events of the past year to drive improvements in how the private credit market operates for trade finance assets.

One area of improvement is in risk controls. One asset manager, speaking on condition of anonymity, says the First Brands scandal had investors “concerned for a little while”.

“They asked a lot of questions and a lot of soul searching was going on,” they say. “But overall I would say it probably helps to have cases like this, because they reinforce the need for discipline. These events have certainly strengthened not just trade finance or working capital, but other corporate lending.”

Maurice Benisty, chief commercial officer at FIS Supply Chain Finance, formerly Demica, points out that as private credit comes under stress, demand for asset-backed lending is likely to increase.

“So though there is an impact on funds facing redemptions, there are also funds with robust underwriting processes and differential access to capital that can ramp up,” he says. “We’re actually seeing more deal flow come in to service.”

Simultaneously, Benisty says wider economic pressures are likely to drive more activity in receivables financing, which – as long as deals are structured properly and subject to rigorous due diligence – are “a safe asset”.

“We are seeing some of the private credit players increase their exposure to such structures,” he says. “You might see a clear-out of companies that are undercapitalised or have early warning signals, but I would expect in 2026 that we will do more deals for private credit as a reporting agent than we would have done in prior years.”

And crucially, while trade finance’s short-term nature could make it a target for redemption requests, it might also prove to be its strength – giving asset managers a way to diversify portfolios by combining liquid and illiquid assets.

“A lot of smart asset managers have always had a working capital component to their private credit business,” says Capolongo.

“We’re seeing a lot of asset managers realising that if they had a more diversified approach and more short-term working capital, they would be in better shape and wouldn’t have to slam down the gates.

“In the long term, that’s going to expand this universe, which is a good thing.”