To fuel the rising demand for digital, defence and energy technologies, mining activity is slated for drastic growth over the next five years. GTR maps out current critical mineral hotspots and deals across the globe.

The mining sector is heading into a period of intense growth as governments and industries race to secure the critical minerals deemed essential to economic or national security and at risk of supply chain shocks.

Some projections suggest the industry could balloon by as much as US$600bn to US$3tn by 2029.

Meeting this demand, however, will require a dramatic increase in supply. Benchmark Mineral Intelligence, a mining analyst firm, estimates at least 384 new mines will be needed by 2035 just to serve the electric vehicle market.

This pressure is already visible in consumption trends. Lithium demand rose by almost 30% in 2024, and minerals such as nickel, cobalt, graphite and rare earths also saw strong growth, according to the International Energy Agency.

The problem is that supply cannot ramp up quickly. New mines can take years to start producing – discovery, development and construction take time, while commodity prices can be volatile and affect project economics.

Processing is also vital. Trafigura’s chief executive, Richard Holtum, told attendees at London Metal Exchange Week in late 2025 that refining and smelting capabilities were more important than mining.

Against this backdrop, commodity traders are using prepayment facilities to secure long-term contracts for vital metals, while governments are forging partnerships and making sizeable investments to lock in access to them.

A global scramble

The concept of critical minerals is nothing new, initially sparked by shortages of raw materials during the First World War.

But as geopolitical allegiances have shifted in more recent decades and supply chain disruptions have become more prevalent, countries have been updating their own national lists of what they consider “critical”.

“Every country has come up with their own list of critical minerals. What is critical for the US is not critical for Europe, and what is critical for Europe is not critical for China,” says Captain Pappu Sastry, chief executive at GSC Consulting, which has recently established a mining advisory division.

These lists differ widely. The US recently added silver and copper, bringing its total to 60 minerals. In the EU, the list has grown from 14 critical raw materials in 2011 to 34, as of 2023.

“Critical minerals that people have never heard of will become very important,” Captain Sastry adds.

These policy lists do not necessarily reflect where minerals are actually produced.

Chile and Argentina “dominate lithium, the DRC has cobalt, Indonesia controls nickel, and China has rare earth processing”, says Alison Allen, EU regional sector leader for mining and mineral resources at SLR Consulting.

“Australia and Canada offer diversified portfolios, which make them attractive. We’re also watching Central Asia, parts of Africa, and increasingly Ukraine,” she says.

“Ukraine has substantial critical mineral deposits and, as reconstruction efforts gain momentum, there’s significant opportunity to develop these resources to support rebuilding the country’s economy.”

“ESG and technical requirements have merged. A technically sound project with poor community engagement is unlikely to get financed.”

Alison Allen, SLR Consulting

In the rush to press ahead with new mining and processing projects, the sector’s poor track record on human rights and sustainability remains a hurdle.

The process of opening up new mines “has to be ethics-intensive”, says Danielle Martin, co-chief operating officer at the International Council on Metals and Mining, an industry body set up to improve the sector’s sustainability.

The organisation is in the process of teaming up with other initiatives like Copper Mark to create a shared standard.

“You can’t change where the metal is, but you can change the governance,” she says.

“ESG and technical requirements have merged,” says SLR’s Allen. “A technically sound project with poor community engagement is unlikely to get financed.”

She adds that consultants are also seeing a growing emphasis on transparency, with investors and original equipment manufacturers demanding traceability back to the mine level.

The need for transparency is also driven by risk, with scams a real possibility, Captain Sastry points out. “We get our own mines proposed to us sometimes. That’s why the due diligence is required.”

But where are all these deals happening? This round-up of big pre-payment facilities, pre-export finance deals and a range of strategic partnerships shows the scale of activity around the world over the last two years.

Africa

Africa boasts some of the richest mineral deposits in the world, with many sites yet to be explored. Central Africa’s Copperbelt spans parts of Zambia and the DRC, while the West African Gold Belt includes Ghana, Mali, Burkina Faso and Guinea.

The continent’s mineral reserves have attracted global interest, from governments to tech firms. According to the African Policy Research Institute, there are almost 100 mineral agreements between African states and international partners centred on resources, like lithium, cobalt and rare earths.

The number of deals done in the DRC shows its value to the leading commodity traders, as well as to mining firms globally. In a Trafigura deal with Ivanhoe, for instance, the trading giant will receive 20% of the mine’s copper anodes over the next three years, while the mine’s Chinese partners, CITIC Metal and Zijin Mining Group, will take the rest.

In July last year, the DRC also signed a framework agreement with KoBold Metals to support the company’s purchase and development of a lithium deposit in Manono. KoBold, which counts Jeff Bezos and Bill Gates among its investors, is banking on AI to help it speed up the discovery of minerals.

Commodity traders are continuing to forge partnerships with African countries to tap into their minerals. In December 2024, for example, Mercuria announced a joint venture with Zambia to finance, buy, sell and export copper.

Yet the development of copper supplies in Africa has been stymied by various factors, Captain Sastry says. “There are mines where the promoters took [out exploration licenses] about 20 years ago, and they have not done anything about it. So the mining licenses have lapsed.”

As these sites are revisited, the economics are shifting. “When you renew all the data and revise all your projections, what was not economically viable 10, 15 years ago is actually economically viable now, because of the growth that copper shows in market size and pricing,” he explains.

Middle East and North Africa

Many countries in the region have a long history of mining and still hold plentiful mineral deposits, from gold in Egypt’s Eastern Desert to Jordan’s phosphate mines. Several also possess untapped reserves, such as Libya’s millions of tonnes of iron ore, used in steelmaking, which has the potential to become big business.

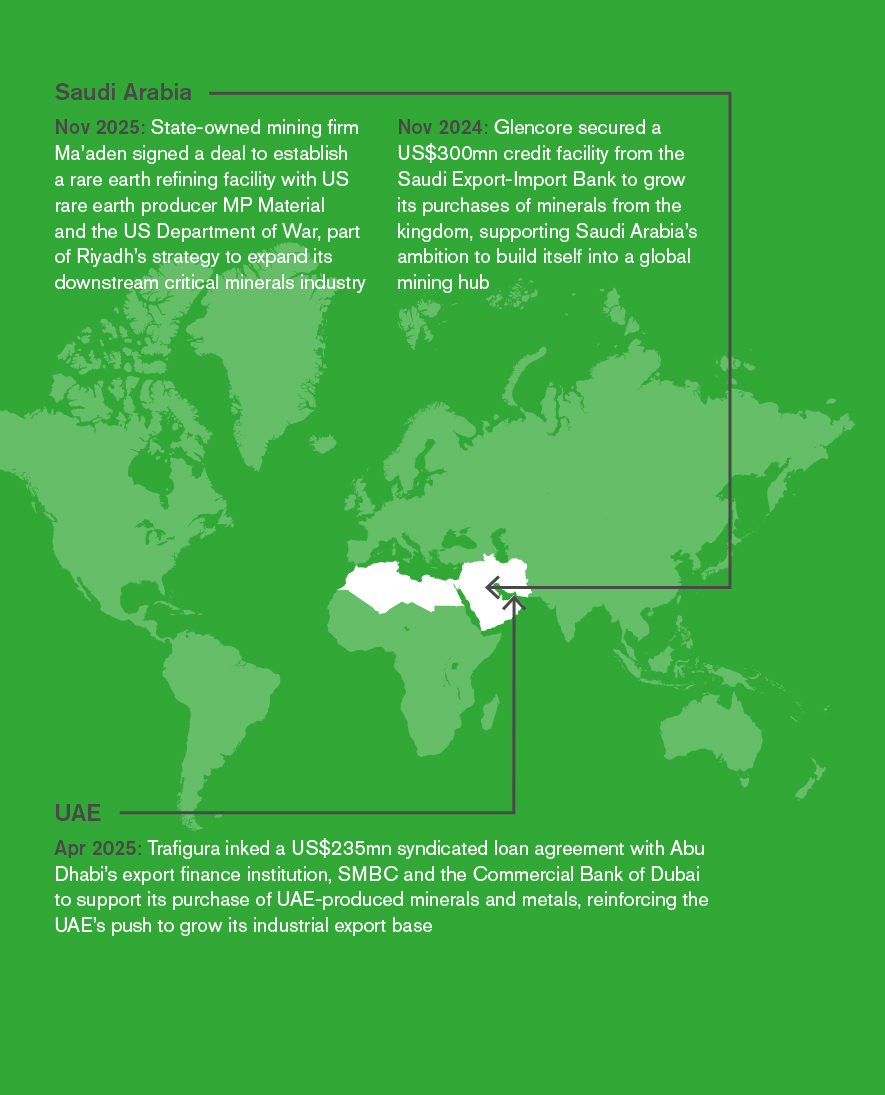

Through its Vision 2030 policy, Saudi Arabia is rapidly increasing its investments in mining projects worldwide, cutting down on wait times for mining licenses and developing its own processing facilities and reserves – including rare earths, which are collectively worth around US$2.5tn.

In Qatar, the state-owned mining company has set up a subsidiary to explore copper and gold in Sudan, while the UAE is developing a mineral resources strategy to increase the sector’s share of non-oil GDP to 5% by 2030.

The UAE’s recent partnerships include the launch of a US$1.8bn consortium with the US and investment firm Orion Resource Partners to invest in existing or near-term lithium, copper and rare earth projects worldwide.

Americas

The US has been aggressively pursuing measures to cut China out of its supply chains and increase domestic production.

Its export credit agency launched a financing mechanism for critical minerals imports to tackle what it called “market manipulation” by China, while an executive order from October outlined a range of measures to curb the nation’s “reliance upon hostile foreign powers’ mineral production”.

In November 2025, US Exim announced it was planning to invest US$100bn in supply chains to funnel minerals, nuclear power and liquefied natural gas into the country, including initial deals agreed with Egypt, Pakistan and Europe.

The nation has also been signing numerous strategic partnerships with its allies to shore up supplies, as well as investing in domestic production. Recent deals include a pact with Japan – also vulnerable to export restrictions from China – to strengthen rare earth processing technologies.

South America features the Lithium Triangle, which comprises western Argentina, northern Chile and southern Bolivia, and holds more than half of the world’s known lithium resources. Chile is also a major producer of copper, with the world’s largest share of reserves and responsible for around 24% of global production.

Innovative initiatives include a venture by Vitol and credit investment firm Breakwall Capital to set up Valor Mining Credit Partners, which aims to make structured credit investments in mining companies across the Americas.

Asia

Australia has been awash with investment and deals for its mining and processing capacity, and is a key player in the US’ attempts to reconstruct its supply chains. Reuters reported in October that US government officials had offered to buy equity stakes or agree on offtakes with the country’s critical minerals firms. The two nations also recently signed a critical minerals and rare earths framework.

Trafigura-owned metals producer Nyrstar was one of the first to receive support under the agreement from Export Finance Australia (EFA) to finance antimony production at its Port Pirie metals facility in South Australia.

EFA previously launched a A$4bn (US$2.62bn) Critical Minerals Facility in 2021, which has helped finance a graphite mining and processing operation, among other projects.

China is continuing its own programme of investment in critical minerals, as are other Asian nations. “Most of our investors are either Indian, Chinese or Indonesian,” Captain Sastry says, discussing investors in the African mines GSC is working with.

“Increasingly, we have also got Australian public-listed companies showing a lot of interest.”

US President Donald Trump wrapped up a tour of Asia in October last year, during which he signed memoranda of understanding with the governments of Malaysia and Thailand to shore up critical minerals supply chains.

The US also agreed to a year-long pause on Chinese rare earth export controls, after restrictions were imposed over the course of 2025. These minerals are vital for making permanent magnets used in cars, wind turbines and data centres. China continues to dominate both the mining and refining stages of the supply chain.

Europe

The EU, too, is aiming to significantly increase its domestic supplies of critical raw materials. By 2030, it hopes to achieve extraction, processing and recycling levels of 10%, 40% and 25% of annual EU consumption, respectively.

Like the US, the EU and the UK have stepped up their partnerships and investments in critical minerals, both at home and abroad. In early 2025, the European Commission approved several strategic projects, including lithium developments in France, the Czech Republic and Portugal.

In March, the Japan Organisation for Metals and Energy Security and energy and metals supplier Iwatani announced they were investing €110mn in a French rare earths refining project. This is another significant attempt to bypass China: Japan is one of the world’s largest consumers of rare earths for automotive and electronics manufacturing, yet relies heavily on Chinese processing.

And in another example of how geopolitics can go hand in hand with negotiations over critical minerals, the US has been keen to secure access to Ukraine’s mineral wealth, which includes rare earths, among many critical resources. In April, the two countries agreed on terms for joint investments in Ukraine’s natural resources as part of the broader strategic partnership between Washington and Kyiv.